Top pharma industry predictions for 2020

The coming of 2020 marks not just the start of a new year, but also of a new decade, when a number of new trends are likely to take shape in the pharma world. Which hot therapeutic areas will dominate pharma industry growth? Which new regions will elbow their way into emerging markets? Will the flurry of fast-paced M&A business deals continue? What equipment innovations are on the horizon? How will the upcoming elections and politics change the landscape of pharma?

For insights on where pharma is headed and what it could mean for manufacturers, we reached out to some of the industry's top experts. Here’s what they saw when they looked into their crystal balls for 2020 and beyond.

Hot therapeutic areas

The market for mAbs will be more democratized

In the traditional space of biologics we will continue to see the democratization of monoclonal antibodies (mAbs). Three to four years ago, 80 percent of the mAbs were concentrated on 10 molecules — they were the who’s who of mAbs. Now, they represent 60 percent and will decline over time. A new generation of up-and-comers — such as the cancer immuno-therapies Keytruda and Opdivo — are on the rise, but also the total number of antibodies is going to be significantly larger. Part of what’s leading to this uptick is that the cost of putting in place a production facility is a fraction of what it used to be thanks to single-use technologies, which will also continue to be used more in the marketplace. There are more niche therapies coming to market, requiring smaller quantities of individual biotherapeutics. This evolution will drive the continued adoption of single-use, which will enable multi-drug manufacturing facilities.

~Andrew Bulpin, head of Process Solutions, Life Science, MilliporeSigma

Ramping up for cell and gene therapy

Cell and gene therapies provide great promise for developing effective patient-specific treatments based on a person’s unique genetic and cellular make up. But these 1:1 therapies come at an incredibly high cost. With more cell and gene therapies expected to be approved in 2020 and beyond, we anticipate this sector of the pharmaceutical industry will continue to ramp up. Scalability and costs will also become focal points for delivering cell and gene therapies and other specialty therapies. Pharmaceutical manufacturers will seek strategies to scale more quickly and drive down costs, and one potential solution may be the development of therapies with common DNA characteristics no longer tailored to one-to-one, but one to many.

~Kevin Lawler, vice president of worldwide sales, Pelican BioThermal

Specialty sectors will drive M&A

Expect oncology to be a fundamental driver for a lot of deal-making activity, as it encompasses over one-third of both pipeline assets and clinical trials. Gene therapy was clearly evident in 2019 deal-making trends and it is not yet too late for newcomers to be making moves in gene therapy manufacturing and discovery, despite the sky-high valuations. It is a trade-off between being first-in-class versus sitting on the sidelines and potentially identifying the best-in-class technologies and most suitable clinical opportunities. We may also see further deals with digital health components such as real-world data, AI-ML and digital therapeutics. Thus far, biopharma companies have predominantly been partnering to add these capabilities to their own operations, but having internal expertise may allow the industry to better face the encroaching threats of large tech companies entering the health care space.

~Dan Chancellor, therapeutic area director, Informa Pharma Intelligence

The rise in new treatments will generate interest in innovative forms of drug delivery

The major trend of new biological treatments is undoubtedly going to continue into 2020. These will be focused on major and severe disease states and challenges of delivery of these complex molecules/systems will still hinder progress. With the increasing demand for higher health standards across all populations, there is likely to be a growing realization that the treatment of moderate conditions using more conventional patient-centric dosages (oral, topical) will remain an attractive market. Particularly in the niche area of topicals, with changes in the industry and new guidances, the need for reliable manufacturing of complex semi-solids can be expected to increase.

One route of delivery which will get increasing attention is the direct route to the brain via the nasal cavity alongside the increasing prevalence of neurodegenerative diseases in the aging population. This route avoids first-pass metabolism and potentially avoids issues associated with the blood-brain barrier. As a consequence, new in vitro tools that can reliability model penetration of drugs through viable human nasal epithelia are of growing interest.

~Jeremy Drummond, senior VP of business development, MedPharm

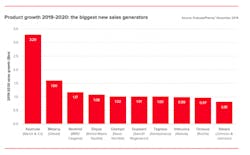

Cancer drugs will dominate pharma growth

Next year, eight drugs are expected to add $1 billion or more in new sales, and four of them are cancer drugs. The ability to charge relatively high prices in oncology helps these products to feature prominently, though it is also true that several of them represent real breakthroughs.

Source: EvaluatePharma Vantage 2020 report

~EvaluatePharma’s Vantage 2020 Preview. Download the full report here.

Industry-wide trends

Looming pricing reform will lead to cost pressure and expanded outsourcing

With increased public scrutiny on the price and accessibility of pharmaceuticals worldwide, there will be continued focus on bringing pharmaceutical prices down, which has the potential to dismantle long-standing pricing models for drug developers. With the upcoming 2020 U.S. election, Congress will likely drive pricing reform — which will impact the development of drugs and specialty therapies and likely accelerate the release of generic and bio-similar versions to the market. In an effort to preserve profitability, pharmaceutical companies are expected to continue expanding the use of outsourced partners to drive down costs. Sales and R&D are likely to be the only functions retained in-house, with all other critical operations in the distribution channel outsourced. As a result, we expect to see more alliances between packaging, transportation and contract manufacturing providers to leverage best-in-class capabilities to support increasingly cost-conscious global pharmaceutical manufacturing companies.

~Kevin Lawler, vice president of worldwide sales, Pelican BioThermal

M&A activity will continue growing

M&A volumes have been steadily increasing over the past few years, and all of the fundamentals are in place for this to continue at its current ~10 percent growth rate. This would leave us with in the region of 260 M&A deals executed through 2020 — one for every working day of the year. It is harder to predict the combined values of these transactions because they are so heavily driven by one-off mega-mergers — I doubt many would have put money on AbbVie combining with Allergan — so it may be that the total values getting exchanged are somewhat volatile.

In particular, we expect several research-stage companies to transition into potential commercial operations as their drugs reach key regulatory milestones, and it is here where larger companies with global scale are best placed to create value. Intercept Pharmaceuticals is certainly one such opportunity should it gain approval for the first non-alcoholic fatty liver disease (NASH) drug, entering a large and untapped specialty market. Other companies making a similar transition have recently been acquired, including Alder Biopharmaceuticals and The Medicines Company.

~Dan Chancellor, therapeutic area director, Informa Pharma Intelligence

Biopharma’s financial market is braced for a rocky ride in 2020

Rhetoric around drug pricing is only going to increase as the U.S. presidential election gets closer, keeping a sector already unpopular with voters under the spotlight. While political gridlock means that U.S. lawmakers are not expected to agree on any new measures any time soon, it is clear that the cost of medicine will remain a live issue next year. This is all likely to translate into a volatile time on the stock market. The IPO window is not expected to completely close next year, but equity investors are probably not going to be as receptive as in 2019. Venture investors too could adopt a more prudent stance towards financings, particularly if it starts to look like their own funds will need to last longer.

~EvaluatePharma’s Vantage 2020 Preview. Download the full report here.

Global changes

Northern Asia will make progress in advanced therapy R&D more quickly than the U.S.

When companies are testing new therapies in an established market like U.S. and EU, they set up clinical trials — meaning they enroll patients and then look at results. But in some countries like South Korea and China, when companies use an advanced treatment like CAR-T cell therapies on a patient, local regulators consider this to be more like a medical procedure. Because of this difference in regulations, companies can more quickly see if the treatment is working and then modify the treatments in a much faster time frame than in the Western world, where companies have to wait for trial results. This will help spur more advances in cellular and gene therapy research in Asia.

~Andrew Bulpin, head of Process Solutions, Life Science, MilliporeSigma

New regions will emerge as leaders in the low-cost generic market

In 2020 and beyond, pharma will see accelerated consolidation of pharma companies and fast growth of emerging markets, particularly in oncology and biologics. With generic pharma running out of ways to reinvent itself, they have few growth opportunities in their traditional markets. Generic pharma consolidation will level out with most companies worth absorbing off the table.

[pullquote]

Emerging regional pharma companies in Europe, Middle East and North Africa (MENA), and the wider African continent will purchase low-profit generic assets. Great investment in this sector is underway in South Africa. Note that most drug products sold in the MENA region are more expensive than in most EU member states.

This will be the African decade where the smart money will be deployed. China has had a 10 year head start in Africa, mainly in the energy sector, and I suspect health care will be the next area of focus for China. Branded pharma will continue to divest its less profitable assets and invest in oncology and biologics drug products. Small molecules will be the battlefield for the startups and small pharma, targeting mostly repurposed drugs. There will be fewer approvals of biosimilars in the U.S. as regulatory hurdles and development costs remain complex and out of reach for most companies.

~Badre Hammond, vice president, commercial operations, Aptar CSP Technologies

Global operations could change business strategies

As markets continue to globalize and global customer demand continues to increase, we’ll see an increased focus in 2020 for establishing global operations strategies. In particular, a holistic operations strategy from pharmaceutical manufacturers is necessary to meet the pharmaceutical industry’s stringent quality requirements, while providing uninterrupted service to patients. It must begin with a complete understanding of customers’ needs and ensuring an engaged team approach to meet those needs. Manufacturers must have an integrated strategy in place with a collaborative focus across the operations pillars of manufacturing, procurement, supply chain, process excellence and advanced manufacturing engineering. Operating within a lean manufacturing business system across these pillars will enable manufacturers to see impactful results in safety, quality, service, and cost efficiencies.

~David Montecalvo, senior vice president and chief operations and supply chain officer, West Pharmaceutical Services

Manufacturing innovations

Notable advances in equipment tech will continue

To support required advances in operational efficiency, machines are going to be smarter. From a tablet press perspective, this means additional sensors to facilitate predictive maintenance, and a full complement of on-board support and diagnostic tools so problems can be quickly identified and remedied. Operator competence will be supported with on-demand content and videos, available from the machine HMI, to supplement procedures for setup, changeover, turret exchange, troubleshooting, and process optimization.

Machines will also be more connected and in some cases looped into a central network, SCADA, or an iHistorian system to ensure that all data — not just the standard process parameters — is captured and available for analysis. This includes audit trails for machine adjustments, press faults and tablet rejects, all of which can be used to assess how the machine is being operated. The result is a deeper understanding of what is happening in the compression suite, and the foundation to optimize both the process and the manner in which the process is executed by the operations team toward the goal of optimized product quality.

~Frederick J. Murray, president, KORSCH America

Supply chain strategies will evolve

The breakthroughs we have seen in the last few years, particularly in the area of cell and gene therapy (CGT), are just the beginning and will bring opportunities to progress from treatment to cure for patients suffering from cancer, diabetes and rare/orphan genetic disorders.

These therapies are a challenge for the established supply chain models and CGT will further drive the development of demand-driven supply chains. These newly designed supply chains will better meet the requirements of smaller volumes, higher-value batches and personalized therapies with a decentralized rather than a centralized manufacturing approach.

A major influence on this supply chain evolution will be patient-centricity with virtual strategies. Virtual trials are often a key part of a patient-centric strategy and the potential benefits where a comprehensive strategy is implemented can be incredible. By leveraging state-of-the-art technologies and processes such as direct-to-patient logistics, wearables, mobile health technologies, big data and AI, clinical sites can mostly be eliminated from the supply chain and patients will become more engaged and active when participating in trials.

~Sascha Sonnenberg, global head of business development, Sharp Clinical Services

Supply chains will become more patient-centric

There’s going to be a shift towards a more patient-centric health care system. Two years ago "patient-centric" was one of those things you needed to have in your business strategy, but it didn’t go anywhere. Now, it is on our doorstep and it’s going to drive digital transformation efforts. It is going to involve branded manufacturers, suppliers, and distributors working on the same network for a patient.

It’s not possible to tie together all of the ERPs to deliver it to the patient — it’s too complicated, too expensive, and if you talk to the manufacturers, they’ll say they're integrated to distributors and wholesalers and can only see that far. But, the health care ecosystem is a platform and that is the basis of digital transform. So platforms that allow multiple partners to connect on the network and onto one platform is patient-centric. The shipper, the speciality vendors, etc, will be on the network. It will involve everybody collaborating in real time, helping health care become a patient-centric network for all platforms. This will also allow companies to increase the safety and traceability of drugs.

~Roddy Martin, chief digital transformation officer, TraceLink

Real World Evidence will become more paramount in drug studies

Real World Evidence (RWE) is going to be become even more important as we move into 2020. In 2019, the industry saw the Food and Drug Administration (FDA) approve the first drug where its analysis was largely based solely on real world data (RWD) with Pfizer’s Ibrance. The demand for RWE is increasing due to the growth of rare disease studies and rising clinical trial costs, as well as the emergence of technologies to capture data outside of a clinical trial and we should expect more RWD within our study protocols.

RWD collected through observational studies outside of the traditional clinical setting holds great potential for rare disease trials where it’s more difficult to recruit for smaller patient populations and fund a full-scale randomized clinical trial.

The correct collection of RWD is essential to facilitate its analysis and prove drug efficacy and this must be factored into a clinical trial at design stage. Clinical Registries and Electronic Health Records (EHR) and post authorization reports are just some of the sources for RWD. It is important for CROs and pharma to have a handle on how to use this data and also to be aware of latest technologies for processing such data. Some examples include Clinical Pipe which connects EHR to EDC systems and Medable where RWD and all other streams of eSource, EDC is centralized in one platform for analysis.

~Thomas Underwood, head of marketing, Quanticate

Regulations will motivate more companies to explore digital solutions

2019 has seen many pharmaceutical firms starting to explore digital solutions to ensure they are compliant with new track and trace regulations and it’s likely that this will continue into 2020. Many serialization solutions require the implementation of new data management systems to collect, store and securely transfer the necessary information between supply chain partners.

Many of the data management systems being introduced into the market use technologies such as blockchain. Blockchain can be used to create an immutable ledger of data, which acts as a digital mirror of the supply chain. New data entries must be verified by other stakeholders in the chain, which not only helps to ensure that products are verifiable at the point of dispensing but can also provide in-depth and real-time analytics can allow companies to react more swiftly to market demand, improve operational efficiency and improve inventory management.

Companies have also started to look at how the new processes and systems they’ve put in place could help to improve auditability and other internal operations as a result of increased access to operational and supply chain data.

~Marcelo Cruz, head of marketing and business development, Tjoapack