Economies of Scale for Manufacturing

Identification of manufacturing scale is an important step in the late-stage commercialization process. It sets the stage for the scale-down operation with end in mind. An appreciation of the economies of scale by engineers and scientists is an important factor in an optimal design. The application of a rigorous economy of scale methodology is important to finalize the scale of operation. This section describes factors that must be considered in finalizing the scale of operation.

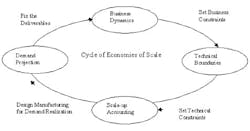

Economies of scale could be represented as a cyclical process, as indicated in the figure below. The initiation point of the cycle is demand projection to understand the business deliverables; this is followed by business dynamics, which in turn set the business constraints. Demand projection and business constraints set the business expectation for the manufacturing facilities, which gets translated into the technical boundaries.

Once the technical boundaries are set, then a scale-up accounting methodology helps achieve the optimal utilization of capital with regard to the demand. Even after a product is commercialized, any changes in demand would lead to repeating this cycle.

Demand Projection

To estimate future demand, the company may use several methods: buyers survey, composite of sales force opinion, expert opinion, market tests, time series analysis/dynamic modeling an/or statistical demand analysis. These methodologies could help define total market potential. This is typically defined as:

where:

- Q = Total market potential

- n = Number of buyers in the specific product/market under the given assumptions

- q = Quantity purchased by an average buyer

- p = Price of an average unit

The number that is most relevant to the economies of scale for manufacturing is:

The manufacturing target sets the plant capacity for producing a particular product. Plant capacity is typically designed in light of future projections and market potential. Various assumptions are used in collecting the data for market potential. These assumptions may range from conservative to optimistic estimates. The dilemma is, should the company create manufacturing facilities based on optimistic estimates and suffer idle capacity, or should it take a conservative course and suffer lost opportunity. Each company has its own philosophy for risk taking.

Business Dynamics

Demand projection gives management enough information to decide whether to launch the new product or not. Commercialization is a significant cost in the product life cycle; therefore, careful financial consideration is key to the economic viability.

If the economic forecast is favorable, the next step is the timing. In commercializing a new product, market-entry timing can be critical. Speed of commercialization is often stressed by companies as a key competitive advantage and is especially important for the pharmaceutical industry due to patent protection aspects.

Location of the manufacturing site is another important issue facing business leaders. Considerations such as taxes and locations are probably significant factors to take into account. Certain locations (e.g., Ireland, Singapore, and Puerto Rico) currently have tax advantages for manufacturing in the global economy. Diversifications of risk or supply chain consideration are also critical in determining whether to manufacture the product at multiple sites or a single site.

Technical Boundaries

The demand projection and business dynamics help formulate the boundaries around the economies of scale. Another vital factor in the economies of scale is the operability of the manufacturing scale under the technical constraints.

These technical constraints may be process or facility specific. The process constraints are determined during the development stage. Especially relevant is the scalability aspect of the process developed. For financial analysis that precedes detailed process development work, typically a very approximate estimation of technical boundaries is made with the help of process experts.

Scale-up Accounting

After setting approximate boundary conditions demand, business dynamics and technical boundaries the challenge is to specify the scale of operation. This is not a trivial task and there is no unique answer.

Scale up in industry has been achieved by and large by trial and error. For example, while some biotech companies have successfully scaled up bioreactors and benefited from the economies of scale, others have successfully used numerous batteries of small-scale equipment to achieve the manufacturing target. A few small-scale companies have gone out of business either because they had an incorrect scale of operation or their competitors had a more efficient scale of operation. Thus, a rigorous financial analysis of scale of operation is critical to the survival of the company.

In scale-up accounting, manufacturing or production costs are critical. They can be classified into three basic categories: 1) direct materials, 2) direct labor, and 3) factory overhead. Direct materials and labor are variable costs. Variable costs are those in which the total cost changes in direct proportion to changes in volume or output, while the unit cost remains constant.

These three categories of manufacturing cost flow through the work in a process inventory account. The costs of direct materials, labor and factory overhead used in production are charged to work in progress. When goods are completed, the total costs incurred to manufacture the goods are transferred from work in progress to the finished goods inventory account.

While the above accounting principles are adhered to in product costing, the scale-up aspect is more sensitive to the fixed and variable cost concepts. Variable costs are key levers in cost control of any manufacturing operation.

Author's Note: The value of the scale-up accounting concept is explained using a scale-up case study in Pharmaceutical Operations Management, a book co-authored by myself and two professors at the University of Newcastle, England: Gary A. Montague and Jarka Glassey. The book is published by McGraw-Hill Professional Publishing. This article is based on an excerpt from that book.