Contract Manufacturing & Development's Big Pharma Ascendency

With 2017’s fourth quarter economic data extremely strong, a new tax bill that lowers corporate rates and unemployment at historic lows, it is likely U.S. pharmaceutical consumption won’t be abating any time soon. The strong sustained growth of North American drug and healthcare consumption only serves to bolster the number QuintilesIMS projects for the world’s drug consumption, noting overall global drug spending is on track to reach $1.5 trillion by 2021.1

Most current statistics point to solid and continued spending on processing and manufacturing capabilities offered by contract development and manufacturing organizations (CDMOs), especially those planning on serving biopharmaceutical and biosimilar customers over the next decade.

As pharma-biotech moves past the first quarter of 2018, players serious about their role in the CDMO space are anticipating positive revenue growth and working their go-to-market strategies because they’ve spent the last three to four years positioning themselves tactically and operationally to pursue the opportunities the R&D pipeline continues to deliver. EvaluatePharma (who projects global pharmaceutical markets expanding at a CAGR of 6.3 percent) predicts R&D spending will maintain 2.8 percent CAGR through 2022 and that spend will add 50 percent more revenue over the same period.

For contract manufacturing and development service companies, opportunities for growth and success in the coming years will be predicated on their ability be strong, globally positioned strategic partners and leading actors on the world stage, which supported a robust level of high-level strategic maneuvering and tactical/operational spending by prominent CDMOs and other surprise players in 2017. Merger and acquisition activity reflected strategic intentions as did the character of operational/capacity expansions.

Looking at what’s driving pharma and CDMO business lately, contract manufacturing leaders continue to initiate organizational and operational strategies to compete for business in the active pharmaceutical ingredient (API) area and capturing more of its value by instituting efficient flexible manufacturing.

Last June, Clarivate Analytics’ Kate Kuhrt set the current API market at $140 billion on the supply side, a data point she presented on API supply and demand at DCAT Sharp Sourcing.2

With demand for API manufacturing support, and completing the development and commercialization pathway for biopharma, healthy growth rates are predicted for global pharmaceutical contract manufacturers. According to the Mordor Intelligence report “Pharmaceutical Contract Manufacturing Market - Growth, Analysis, Forecast to 2022” published October 2017, the market for contract manufacturing was valued at $65.10 billion in 2016 and is projected to reach $94.38 billion by 2022, during the forecast period from 2017 to 2022.4

However, to deliver the continued gifts of the pipeline to patients and consumers, contract services providers must also be able deliver on the rising curve of what good manufacturing practice is relative to manufacturing capability, and the operational excellence necessary to compete and win the development and manufacture of new, highly lucrative therapeutics on the global stage.

Drugs of all types are growing more sophisticated and tougher to manufacture without error. From small molecule formulations with time-release or anti-abuse features, to sophisticated biologics and personalized genetic treatments to popular biosimilar equivalents, all are headed for burgeoning global markets.5

Drug manufacturing complexity is also compounded by other factors including the arrival of highly engineered drug delivery devices and primary and secondary packaging that has as much to do with the value and effectiveness of the therapy as the API. Packaging in its own right echoes the larger contract services universe as its role in providing for the safety and security of the world’s pharmacy grows more complex and critical each day.6

Most in the industry are well aware of the challenge of providing safe, affordable and effective drugs, cost effectively. Big pharma is certainly driving the contract manufacturing supply chain. But the reasons for outsourcing more of everything to CDMOs have changed in response to competitive and socio-economic market forces driving drug consumption and regulation.

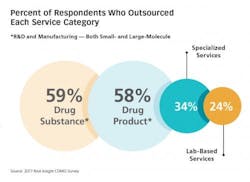

Nice Insight gathered input from more than 700 pharmaceutical industry professionals from across pharma (41 percent large, 36 percent medium-sized, 20 percent small and 3 percent emerging) and around the world (38 percent in the EU, 33 percent in N. America, and 29 percent in Asia). Results from the 2017 Nice Insight Contract Development and Manufacturing Survey offers insight into why the CDMO’s role in pharma-biotech has become so prominent and critical: The top reason survey participants engage CDMOs and contract services providers is “access to specialized technologies.”7

Parenterals big Production

Respondents are also seeking to improve quality and gain expertise in operational areas their organizations may not be as strong in delivering cost-effectively. Nice Insight CDMO survey data revealed that more than half (54 percent) engage contract providers for liquid dose form clinical-scale and commercial-scale drug product manufacturing services.

Further, roughly a quarter of respondents engage CDMOs for clinical-scale and commercial-scale filling of prefilled syringe and injectable dose delivery forms; it is no wonder considering what it takes to accomplish sterile operations with zero quality excursions at commercial capacities.

Philippe Mougin, Chairman of Cenexi Group, commented that patient safety relies heavily on error-free fill/finish operations. With their inherent complexity to manufacture and finish, biopharmaceuticals are propelling the use of parenterals, which Mougin notes are expected to make up approximately 17 percent of the packaging market in coming years.8

Spending for Quality, Capacity and Capability

Among the contract development and manufacturing services companies responding to the expanding demand for capacity and technical ability during 2017, there was strong evidence that investment and capital allocation strategies are ongoing in support of long-term goals.

One of the most interesting deals to emerge in 2017 was Thermo Fisher’s acquisition of Patheon for $7.2 billion. Can the whole entity create value greater than the sum of its parts? Thermo Fisher has bet that the union will.

All of this follows on Patheon’s M&A activity over the past two years, which had the company pursuing increasingly competitive positions in API services, formulation and drug-product manufacturing capacity.

The Lonza-Capsugel acquisition for $5.5 billion was another benchmark deal, which closed in July 2017. According to the company, the acquisition aligned with Lonza’s strategy of accelerating growth and delivering value by complementing its existing offerings.

Catalent, already a pioneer in sterile fill/finish with Blow-Fill-Seal innovation, announced in September 2017 the acquisition of Cook Pharmica for $950 million. The company explained the move was intended to bolster its biologics abilities and extend its “capabilities in sterile formulation and fill/finish across liquid and lyophilized vials, prefilled syringes, and cartridges.” This follows Catalent’s acquisition of Accucaps and its softgel capabilities in 2016.

Other notable high-dollar deals came through in 2017 (including AMRI and Parexel’s move to private financing) and spending on operational readiness and capability was similarly robust. DCAT reported on 18 announced expansions in a very thorough accounting of activity by March 2017, noting investment by a subsidiary of WuXi; a collaboration between Lonza and Sanofi; a new gene therapy facility for Brammer Bio and expanding filling and lyophilization operations at Alcami among others.9

Vetter also announced significant expansion of its logistics capabilities at its Ravensburg, Germany site as well as consistent articulation of its manufacturing strategy to meet global pharma’s terms, announcing continued investments to expand fill/finish capabilities, including a $320 million investment over 10 years to its Des Plaines, Illinois site.

Pfizer’s CMO Pfizer CentreOne announced in February 2017 the successful expansion of its fill/finish services at the company’s Kalamazoo, Michigan site. The company also announced it was expanding HPAPI contract manufacturing service offerings its Newbridge, Ireland facility which it acquired and is now part of the contract manufacturer’s network. Along with vial-filling of small molecules and biologics, the new Michigan operations expand Pfizer CentreOne’s service portfolio and provides new capacity for filling sterile suspensions.

Similarly, Grifols has added significant form-fill-seal capability to its operations in Spain and is currently working on building a new plasma fractionation plant in Clayton, North Carolina. Construction began early 2017 and the facility is scheduled to start production by 2022.

A Performance Worthy of the Industry That Delivers It

The risk and consequences of business decisions made prior to having all the facts can be daunting—but part of being successful in contract drug manufacturing and development business appears to be exercising the ability to provide high-performance, flexible capacity prepared to support multiple drug development programs simultaneously.

There is a new division of labor emerging in the post- blockbuster drug development and manufacturing arena and the success of the entire industry is becoming increasingly dependent on the CDMO sector.

Will current trends in M&A, expansion and growth strategy be sustained? The past year saw renewed emphasis on consolidation to meet the market on its own terms and its increasing need for contract service providers to physically provide all the means necessary to develop and commercialize their molecules and formulations successfully.

General global pharmaceutical consumption and market growth is projected to continue and recent economic policy news means there may be more capital to fund an even stronger wave of R&D in the coming years. Fortunately, CDMOs and contract manufacturing service providers have been preparing for their leading role and are well prepared to help pharma develop its discoveries into real-world, life-saving therapeutic successes.

References

1. Outlook for Global Medicines through 2021. QuintilesIMS Institute (Dec 2016).

2. Van Arnum, Patricia. APIs: Evaluating Supply and Demand. DCAT ValueChainInsights (July 2017).

3. Global API Market - Growth, Trends & Forecasts. Mordor Intelligence (Dec 2017).

4. Pharmaceutical Contract Manufacturing Market - Growth, Analysis, Forecast. Mordor Intelligence (Oct 2017).

5. Downey, William. Biopharmaceutical Contract Manufacturing Market. Contract Pharma (June 6, 2017).

6. U.S. Remains Largest Market for Pharmaceuticals and Medical Devices. PMMI (Nov 6, 2016).

7. The 2017 Nice Insight Contract Development & Manufacturing Survey

8. Mougin, Philippe. Harnessing CDMO Expertise for Fill-Finish and Inspection of Sterile Pharmaceuticals. American Pharmaceutical Review (July 29 2016).

9. Mirasol, Feliza. CDMO/CMO Expansion in Parenteral Drug Development and Manufacturing. DCAT ValueChainInsights (March 14, 2017)