Risks and Rewards in the U.S. BioSimilars Pipeline

Many companies will soon be marketing a variety of competing biosimilar products for the U.S. and other major markets. Yet specific guidance from U.S. regulatory authorities is lagging, and this is creating disruptive pressures. Congress has recently pushed the FDA to release guidance documents on biosimilar drug approvals. A group of senators wrote to HHS in August about the implementation of the “Biologics Price Competition and Innovation Act” (BPCIA), enacted in 2010 to push the FDA for a framework to review and approve biosimilars. Although the FDA just recently accepted the first biosimilar application for review (Sandoz), it has not released specific guidance. This delay has heightened concerns about just exactly how biosimilars will affect patients, insurers, the drug companies and even suppliers.

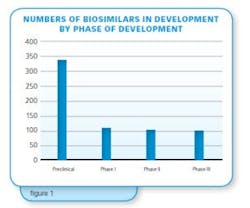

Research in biosimilars and the industry for more than 25 years indicates among the roughly 4,500 biopharmaceutical candidate products in the pipeline, around 20 percent of those products — about 900 — are follow-on biopharmaceuticals, mostly biosimilars (>500), but also biobetters. In the course of Bioplan Associates’ studies, analysis shows only a percentage of these will make it to the market.

PRICING MODELS POORLY DEFINED

Along with the attrition rates for biosimilars candidates, factors such as prices and discounts for biosimilars (relative to long-established reference products), remain poorly defined. These questions may well determine success or failure of biosimilar products in the United States. Biosimilars competition will include multiple biosimilars that sooner or later will be competing for each major biosimilars reference product target, and with other products for the same indication. But how many biosimilar players and products will there be in the U.S.? Will there be too many products competing for sales in relatively small markets or disease categories?

To better understand the issues at hand, what follows focuses on genuine biosimilars, those approved through a formal biosimilars regulatory mechanism involving rigorous analytical and clinical testing to prove biosimilarity. The discussion does not include the perhaps 200 biogenerics, (by regulated country standards), now available or being approved in lesser-regulated international commerce¹.

EU MARKET EXPERIENCE

The current market for biosimilars remains rather small and under-developed, with the U.S. not yet involved. To date nearly all biosimilars market development has occurred in Europe, with smaller biosimilar markets developing in Australia, Japan and other highly developed, highly regulated countries. The global market for biosimilars is only about $500 million, on the order of 1/10th the market of just a single major targeted reference blockbuster (≥$1 billion/year) product. With over a dozen biosimilar products approved in the EU, the average market for each biosimilar is trivial by most standards. Despite biosimilars being approved in the EU since 2006, most European countries have moved slowly in adopting biosimilars. Overall, in EU and other countries, biosimilars are priced at about 25-30 percent discount relative to their reference products.

But it is still early in the game. There are currently nearly 40 blockbuster (>$1 billion/year sales) recombinant protein reference products, with 60 generating sales over $.5 billion, prime targets for biosimilars development. Most of these reference products have patents expiring starting in a year or two, a time when a flood of applications can be expected (discussed below).

EU EXPERIENCE NOT RELEVANT

For a number of reasons, many involving politics and some countries’ centrally managed healthcare systems, the EU experience with biosimilars market development can not be readily extrapolated to the U.S. Uptake and adoption of biosimilars in the EU has been slow, with Germany the only country with biosimilars capturing significant market share from innovator reference products. This is partly due to the reason that government regulations establish quotas for physicians, requiring them to prescribe biosimilars. European market development has been slowed by the diffuse nature of this market, e.g., with 28 different countries being members of the EU. EU biosimilar approvals still have to be adopted by each member state, along with guidelines implemented for use and insurance coverage; all this complicated by many European countries controlling prices and having socialized health care systems. In these contexts, the EU experience in biosimilars market development is not relevant to U.S. market development, where the market is much more open and competitive.

As is normal with pharmaceutical pipelines, most products are in the earliest stages of development, with most yet to enter clinical trials. Essentially, all of these products are targeting the U.S and other major markets. Over 300 companies worldwide are already involved (in various aspects, e.g., development, marketing agreements). Most of the companies involved in biosimilars are either large international (bio)pharmaceutical companies or small new and foreign-based entrants. Classic venture capital-funded and other mid-sized biotechnology-type companies are generally not involved in biosimilars, with these companies targeting new, innovative products. Small company biosimilar developers can be expected to license product marketing to larger established marketers. So at least in terms of marketing, current major players will dominate the U.S. biosimilars scene, at least marketing, in the early years.

ALTERNATIVE EVOLUTION

The U.S. market will evolve differently than the current biosimilars market in Europe. Biosimilars, like generic drugs and other follow-ons, will be priced at a discount relative to their reference product. Uptake of biosimilars will be rapid, with insurance companies and other payers essentially forcing patients’ use of cheaper biosimilars, much as they do with generic drugs.

The U.S. market is attractive because the U.S. will become the largest market for biosimilars, likely surpassing current European and worldwide biosimilars sales as the first few products capture market share. Compared to Europe, the U.S. market is more open, free-market, with more aggressive competition and rapid market uptake likely for any substantially discounted biopharmaceuticals. FDA still needs to implement a number of guidelines and regulations concerning biosimilars approvals. This is causing many companies to go slow in their biosimilars development, particularly including holding off on starting clinical trials directed to U.S. approvals, until FDA makes its own plans clearer.

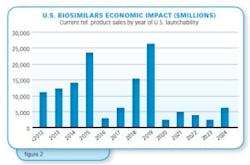

The likely timeline for the economic impact of biosimilars introduction into the U.S. market is shown in Figure 2. The bar chart shows the cumulative 2013 worldwide sales of reference products vs. their expected year of launch in the U.S. (expected reference product patent expiration). Collectively, the data shows that reference products with about $100 billion in current worldwide sales will soon be subject to biosimilar competition in the U.S. market. A wave of significant U.S. market filings and launches can be expected to start next year with another peak in filings and launches (patent expirations) by the end of the decade.

TOO MANY TO BE PROFITABLE?

Once FDA provides appropriate guidances, biosimilar approvals will progress in an orderly fashion, although patent disputes will likely occur with every product, following the pattern with generic drugs. With blockbuster reference product manufacturers making up to tens of millions of dollars in profits, sometimes simply stalling biosimilar market entry for a single day could be well worth pursuing.

How many biosimilars for any particular reference product will enter the U.S. market? Most analysts extrapolate EU market evolution to the U.S., citing it likely that only a few, 2-4 biosimilars at most, will enter the market for each major reference product. We believe there will be more competition in the U.S. market. Already many large international companies, including major biotechnology players (Amgen and Biogen-Idec, for example), most Big Pharma and large generic drug companies, as well as many foreign companies are developing biosimilar portfolios targeted primarily for the U.S. market. These companies expect to be long-term players in the U.S. and world biosimilars market, with most planning to have a portfolio of biosimilars and/or include add these to their present portfolios. For many new, including foreign biosimilar developers, biosimilars will be their entry into the U.S. and world biopharmaceutical markets, and they are determined not to miss this opportunity.

FIERCE COMPETITION AHEAD

We expect more biosimilars entering the U.S. market for each major reference product. If Big Pharma, established biopharmaceutical and generic companies, new U.S. entrants and overseas firms all develop a biosimilar for each major reference product to the U.S., it will create a very tight biosimilars marketplace. Also, there will be biobetters of the established innovator and other products for the same indications will all be competing against each other in the marketplace. Competition could be fierce.

How much will biosimilars cost, i.e., be discounted relative to their reference products? Most, based on European experience, presume that U.S. prices will be similarly discounted by up to 30 percent. However, the U.S. market is a larger, more unified, faster-moving, open and competitive. Economics will drive rapid adoption of biosimilars in the U.S. with insurance companies and other payers going for the cost savings biosimilars will provide. Already, a major player, Samsung Bioepsis, a joint venture of Biogen-Idec and Samsung (development and manufacture) and Merck & Co. (marketing), has announced its intension to launch its biosimilars in the U.S. at 50 percent discount. We project that this will become the standard biosimilar discount in the U.S. Note this is much less than the common ~90 percent discount for many generic drugs. With so much competition, biosimilar companies will have no choice but to efficiently manufacture and market their products.

Will there be price wars? Perhaps. A number of biosimilar developers appear intent on getting their products into the U.S. market, including many international players choosing to mark their entry into the world biopharmaceutical markets, via the biosimilars channel. Many companies, including those well established in the U.S. market, may be more concerned with gaining approvals, market share and building their portfolios, than with maximizing profits from a few early biosimilars. Such companies might try to “buy” their way to market share, and become the spoilers prompting price-war battles.

PROFIT POTENTIAL

Will biosimilars be profitable in the U.S.? Yes, they will be, with markets collectively worth tens of billions of dollars soon becoming available. But markets for most products will be small, compared to their reference products. For example, Abbvie’s Humira is on track for annual sales of about $10 billion/year. Capturing just five percent of this market, $500 million/year, is certainly an attractive and profitable endeavor. Even attaining just 10 percent of a $1 billion market (e.g., having one of 10 competing biosimilars, selling $100 million/year) would be financially attractive, particularly for companies with a portfolio of biosimilars or other complementary products targeting the same indications.

A large number of biosimilars, most targeting the U.S. market, are in various stages of development. The U.S. market for biosimilars will be initially chaotic, with many products and players, including many new to biopharmaceuticals and the U.S. market. There will be many biosimilars for each reference product, with prices generally discounted up to 50 percent. Those companies that efficiently develop, gain approvals, manufacture and market their biosimilars will be profitable. Biosimilar sales and profits will be much smaller than with innovative products, but those in for the long haul, those that best adapt to likely chaotic U.S. market conditions, will be among the winners.

REFERENCES

1) Rader, R.A., “Biosimilars in the Rest of the World: Developments in Lesser-Regulated Countries, BioProcessing Journal, 11(4), Winter 2013/14, p. 41-47.

2) Rader, R.A., BIOPHARMA: Biosimilars/Biobetters Pipeline, database at www.biosimilarspipeline.com