China's Biopharma Growth: Can it Continue?

China is a relative newcomer to the biopharmaceutical industry. Biological therapeutics by multinational corporations in China have been on the market only since the 1990s,1 but the country has been making rapid and significant progress ever since.

The sales of biopharmaceuticals in China’s market grew from $9.4 billion to $22.8 billion from 2012 to 2016 — nearly 25 percent annually. BioPlan’s newly released report, “Advances in Biopharmaceutical Technology in China,” estimates that the market will continue to grow at this rate — meaning that by 2021, the sales volume is expected to reach $48.8 billion. This far surpasses the growth rate in North America, Europe and Japan.1

What does China need to do to continue on this upward path?

BRIDGING THE GAP IN THERAPEUTIC MABS

Multiple sources identify a major gap between China and the rest of the world with regard to the use of therapeutic monoclonal antibodies (mAbs). These products make up a large percentage of biologics globally, but only seven percent of the Chinese biologics market. So far, of the nearly 70 mAb therapeutics approved in the United States, only 12 have been approved by the Chinese Food and Drug Administration (CFDA) and made available in the Chinese market.2

Analysts attribute the gap to several factors:

• For many Chinese patients, the price of imported mAbs, even biosimilars, can put them out of reach, as the national health insurance does not cover many of them.

• There is a lack of biosimilar mAbs from domestic drug makers, which tend to be cheaper.

• It is widely accepted that biosimilar/better drugs from domestic drug makers will be more likely to be put on the National Reimbursement Drug List (NRDL) and made more affordable for Chinese patients, thus holding strong potential for growth in the next decade.

ROBUST SERVICE SECTOR GROWTH

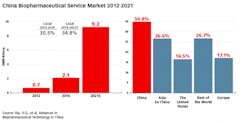

China’s biopharmaceutical service sector, including contract manufacturing organizations, has been growing at close to 30 percent CAGR, and is projected to reach $1.4 billion in 2021.¹ Although there are presently many regulatory hurdles for CMOs in China, these are being resolved, and this segment is demonstrating growth, including the establishment of a number of international and domestic manufacturers in recent years.

There are a number of major driving forces pushing the robust growth of China’s biopharma industry. These include:

Economic development: China’s reform and open-door policy has led to robust growth of the general economy, and ascension into the World Trade Organization has made China, in many ways, the world’s factory. In terms of GDP, China is currently second only to the U.S., representing 19.7 percent of the world’s economy.2 Strong economic development has enriched the quickly expanding middle class in China. Greater purchasing power has made therapeutic biologics less of a luxury for the Chinese middle class, who tend to pay more attention to health issues.

Rising healthcare expenditure; enhanced reimbursement policies: China has become older and richer, and healthcare reform has increased accessibility to insurance and reimbursement for hundreds of millions of people. According to the head of the Ministry of Human Resources and Social Security, Ying Weimin, Urban Residents Basic Medical Insurance, Urban Employee Basic Medical Insurance, and new rural cooperative medical systems combined covered China’s 1.3 billion members in 2015.

Meanwhile, commercial healthcare insurance is also getting more popular among the middle-class urban population. Projections have been made that show commercial healthcare insurance in China will more than quadruple from 2015 to 2020. Total healthcare expenditure in China more than tripled over the past decade. These trends lay a solid foundation for the growth of the biological therapeutics industry.¹

New biological therapeutics from international and domestic drugmakers: In the past two decades, dozens of biological drugs have been launched in China, from both multinational corporations and domestic drugmakers. These include cytokines, enzymes, recombinant vaccines, insulin and its analogs and therapeutic mAbs.

CAN THIS GROWTH CONTINUE?

The Chinese industry will likely keep growing, but may have difficulty maintaining a double-digit CAGR over the next decade as economic development cools and enters a “new normal.” With healthcare expenditure growing faster than economic growth, there is concern that the national healthcare insurance fund has reached or will soon reach overdraft status. Therefore, the Chinese government has made control of healthcare expenditure a policy priority.

In November 2015, the State Council issued a decree to control of the increase of healthcare expenditure from public hospitals (the Chinese healthcare system is still dominated by a public hospital system). Other policy moves include more stringent compliance standards, price negotiations with drugmakers by the Ministry of Human Resources, and “zero markup” for drug prices at hospital pharmacies. All these will put pressure on biopharmaceutical sales, and as was the case with Roche’s Lucentis, many new biological therapeutics may need to have reduced prices to get on China’s National Reimbursement Drug List (NRDL). It is highly possible that revenue from biopharmaceutical therapeutics will maintain a healthy growth rate, but a lower profit margin.

CHINESE PHARMA MOVES TO BIOLOGICS

With the new State Drug Administration (SDA) reforms streamlining the approval process of new drugs originating overseas and the launch of biosimilar versions of mAbs by domestic companies, the structure of China’s pharmaceutical consumption will shift toward a greater market share of biological therapeutics, especially more complex molecules. Although China is still an under developed market in this sector, the penetration rate, especially of the more complex biologics, will increase. Multiple sales statistics show that the biopharma market grows faster than the pharma industry as a whole, and that mAb therapeutics market grows faster than the biopharma market. BioPlan’s internal research also shows that China is likely to approve new gene therapy/cell therapy products in the next decade, since dozens of them are already at the clinical trial stage, although possibly only after the approval of such products in the U.S. and EU.

CHINA'S EXPORT AMBITION

Besides the growth of China’s domestic market, biopharma manufacturers are strongly motivated to export their products to the global market, including the regulated market in the U.S. and EU. BioPlan’s 2017 research, including interviews with 50 biopharmal manufacturing executives in China, confirmed that the country is making efforts to become a global contract bio-processing hub.4 Multiple executives from CDMOs in the industry, including Dr. Li Zhiliang, CEO/founder of AutekBio, are confident that biopharmaceutical will be the next sector that China will lead as a contract manufacturer. As Zhiliang puts it, “This industry is not unique at all. What has already happened in the textile, toy, and mobile industries will happen in the biopharmaceutical sector as well.”

With government subsidies and an influx of returning scientists, contract manufacturing of biologics in China has the potential to offer a cost advantage for global biopharma companies, which will see multiple therapeutic biologics go off-patent in the next decade. Outsourcing the manufacturing of these older products will also enable companies to focus on developing core products.

Despite its relatively late start, a number of major driving forces are pushing the robust growth of China’s biopharma industry, as well as driving the country’s efforts to become a global contract bioprocessing hub.

References

1. Xia, V.Q., et al, Advances in Biopharmaceutical Technology in China, 2nd edition; Society of Industrial Microbiology and Biotechnology and BioPlan Associates, Inc., October 2018.

2. Trading Economics. China GDP. 2018.

3. Barton, Dominic, et al, Mapping China’s Middle Class. McKinsey Quarterly, June 2013.

4. Langer, E.S., et al., 15th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, BioPlan Associates, Inc., April 2018.