Dont Fumble Your Tech Funding Opportunity

Most senior and executive managers in pharma feel they have already made huge capital investments in high technology, and just can’t see the business benefits these investments have delivered.

They point out that, during the approval process for most capital investments, applicants predict very strong ROI, but once the project is up and running the promised returns can’t be documented.

This is a huge problem. Either the investments are realizing benefits that are not discernable, or they are not realizing benefits at all. Usually, it is a combination of the two.

Econ 101

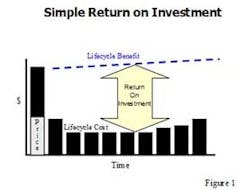

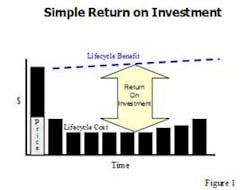

To analyze the issue, it is helpful to review the basics of capital project economics. Figure 1 presents a classic capital economic profile. The bar chart represents the costs associated with the capital investment over its useful life. The dashed line represents the business benefit realized from the investment. Return on investment is simply the integral of the benefit minus the integral of the cost.

I was recently involved in an analysis of a number of completed industrial plant automation projects. In almost every case, plant personnel could determine the cost of the technology over its lifecycle, but had almost no idea of the actual benefit it provided. The cost accounting systems that should have provided this information couldn’t or didn’t, because in industrial operations these systems have typically been designed to support the financial reporting requirements of the organization and not its operational management. Because of this, most cost accounting systems used today report monthly, plant-wide cost and margin information.

Since so many activities occur in any industrial plant over a month’s time, it is impossible to determine which component of any financial improvement or loss should be attributed to any specific activity, even to automation system improvements. Today’s cost accounting systems lack both the timeliness and process-detailed information to effectively measure the benefit from technology. From a business manager’s perspective then, most technology investment requires a leap of faith: It’s a cost with no evidence of discernable benefit.

The key word in the previous sentence is “discernable.” A few decades ago, the business value of most technology investments was clear and measurable—usually just a matter of evaluating headcount reduction brought on by new automation systems. Over the last decade, however, it has become apparent that plants can’t cover the cost of technology simply by reducing heads.

There just aren’t enough heads left. The value of technology investments must now be determined by variables other than personnel reduction cost. Unfortunately, with the current cost accounting systems, this is almost impossible to do.

New Tech, Same Function

An additional problem for pharmaceutical manufacturers is the “replacement technology” mindset, which wants to acquire new technology only to replace the exact functionality of the aging technology. If, for example, an installed control system begins failing on a regular basis and replacement parts become increasingly expensive and hard to find, the owner issues a request for proposal specifying a replacement system that does exactly what the aging system did. Even though the newer system would likely offer considerably improved and expanded functionality, this typically would not show up in the initial requirement for the new system, so the new functionality is never tapped and little, if any, business benefit results.

In the pharmaceutical industry, regulations and validation issues exacerbate the replacement mindset. Tight regulations combined with the cost of validating functional changes in the installed technology systems significantly suppress the inclination for continuous improvement. The FDA’s emerging process automation technology (PAT) guidelines are aimed at alleviating this constraint, but it is still very much a concern in pharmaceutical manufacturing operations today.

Replacing old technology with new technology that does the exact same thing seldom delivers business benefit. From that perspective, it might be a good thing that accounting systems can’t measure business benefit. No one would ever be able to justify any technology investment, and that would be of great detriment to all business operations.

It is not that plant managers don’t know that the new system offers more capability than the one being replaced. They just figure they will take advantage of it once the system is installed. But that seldom happens. One reason is that the technology expertise of the project team leaves once the project is commissioned and the remaining talent does not always have the capability to utilize the new functionality. Another reason is that engineering staffs in pharmaceutical plants have been downsized to the point that they are just trying to keep the plants operating and seldom have time to consider the untapped potential of their technology. The net result is that often less than 40 percent of the available functionality and capacity of installed automation and information systems is actually used during the systems’ life. This represents huge lost opportunity and contributes to senior management’s reluctance to invest in technologies that offer great benefits, but whose potential is seldom realized.

A final issue: Most pharmaceutical manufacturers do not apply a continuous improvement approach to technology investments. With all of the talk and investment in continuous improvement programs such as Total Quality Management, Six Sigma and Lean Manufacturing, it would seem natural that these concepts would be applied to generating business value from technology, but I have yet to find a company that is effectively applying their continuous improvement culture to technology investments.

Project teams are primarily measured only by on-time, on-budget delivery, which tends to reward behaviors that are diametrically opposed to continuous improvement. For example, if there is a system that might provide significant business benefits that are not within the initial specifications of the RFP, few project teams will think about implementing it. It is just not their job. Somebody else is responsible for getting new benefits from the technology, but who? The project team has the expertise, but not the inclination. This is a major cultural and performance measurement issue that must be resolved if senior managers are going to start warming up to technology investments and realizing the associated benefits.

Given these challenges, it is no wonder senior management has difficultly investing in new technology. In today’s difficult economic environment, if the business value from technology investments is not both significant and visible, we should not expect senior management to invest.

Real-Time vs. Monthly Accounting

Convincing senior management that investments in technology are good and important to the business of the company will require a fairly significant paradigm shift. It begins with finding a way to make the benefit from technology investments visible. This requires reworking the approach to cost accounting commonly taken in pharmaceutical operations to include real-time accounting of the benefits, as well as the costs. This may seem beyond the authority of most plant personnel, but it really is just an extension of calculations that automation system platforms have performed for decades.

When cost accounting was introduced to manufacturing operations at the dawn of the industrial revolution, it utilized a bottom-up approach that accounted for each product component as it was produced. As industrial machinery, such as the power loom in the textile industry, helped increase volume and production, accounting for the cost of each piece became impossible with the technology that was available at the time. So instead of accounting for each piece as it was produced, companies looked at monthly totals, closing the accounting books at the end of each month and measuring results then.

Monthly accounting was a difficult but necessary compromise, and after some time the compromise became the normal way of doing business. People earned college degrees in how to make monthly accounting approaches work. When computer technology was introduced to manufacturing, finally making it possible to go back and account for manufacturing operations in real time, most accountants were too set in their ways to take advantage of it. Monthly accounting is the commonly accepted practice, and that is that.

Fortunately, most major pharmaceutical manufacturing operations are already using automation systems that receive real-time operating data from plant-floor instrumentation. Viewing such data in the context of financial models that plant accountants might develop for each process unit, plant engineers with accounting training can model business performance, in real-time, right in the automation systems.

The exact same approach can be extended to develop automatic real-time models of all key performance indicators (KPI) of the enterprise. The output of these models can be historized into standard process historian to produce hourly, shift, daily, weekly and monthly trends of plant accounting. With these in place, the benefit from automation in the capital lifecycle economic model becomes both measurable and visible within the operation. Real-time accounting and real-time KPIs provide the first step in enabling the paradigm shift required to justify technology investments.

A Business Value Approach

The second requirement for the paradigm shift is that we move from a replacement technology approach to a business value approach. This requires pharmaceutical companies to restructure their traditional approach to capital projects, to consider additional value the replacement technology provides early enough in the capital project and to adjust the RFP process. Pharmaceutical companies must recognize and empower project teams to do more than keep to time schedules and budgets; they must also be recognized for the incremental business value they generate. With real-time accounting and KPI models in place, it becomes easy to measure the before-and-after conditions in the plant for every project. The value the project team generates is clear and measurable. If senior management uses this to incent project teams to drive improved business value, the value will come.

But the improvements must not stop with project completion. Once the project team has moved on, a continuous improvement environment must be sustained. This can be easily accomplished by using real-time accounting models and real-time KPIs as the basis for a real-time feedback mechanism for every person in the operation.

Contextualized dashboards (Figure 2) for each frontline operator and maintenance person, each engineer, each supervisor and each manager can be developed to empower every person to make good decisions that continuously drive business value improvements throughout the operation. When the measures are strategically contextualized to each person’s job, they are referred to as dynamic performance measures (DPM). Many pharmaceutical manufacturing operations have tried to develop dashboards for their plant managers, but it is the frontline operators and maintenance personnel that drive the second-by-second performance of the operation. Industry has to start thinking of these frontline workers as performance managers who are responsible for continuous performance improvement.

Changing the Paradigm

The combinations of real-time performance measures based on real-time accounting and KPIs, business value-based technology project execution, and continuous improvement through performance managers truly defines a totally new paradigm for pharmaceutical manufacturing operations. Making this shift a reality calls for a huge cultural change that requires two things.

The first requirement is strong leadership. Senior management must not only be part of this change, they must take ownership of it. The second requirement is providing and supporting the right measures of performance for each person in the operation. This is exactly what the contextualized dashboards do, and the performance measures on these dashboards are available in real time, the necessary time frame for the manufacturing industry.

Although this culture change and approach are fairly new to industry, where they have been applied, the results have been much better than anticipated. On average, programs executed in this manner have provided 100 percent returns on capital investments in less than three months. But that is just the beginning. The continuous improvement culture enables operators, maintenance workers, engineers and managers to drive value improvements and huge cash flow gains from all manufacturing assets. On top of this, the continuous value improvement culture creates pride among all operations personnel and encourages cross-silo collaboration, which drives even more value.

It is true that senior and executive management have been reluctant to invest in technology, and for good reason. Technology investments have traditionally come up short on the discernable business value they were supposed to generate. If the pharmaceutical industry continues on the path it has been on, the reluctance to invest in technology will most certainly increase. The good news is that technology investments can create significant and visible value. Proving to management that technology investments are worth the cost is critical, but it requires a fundamental shift in the way we deal with technology. This change can enable effective dynamic performance measures, performance project approaches and implementation of a continuous business value improvement culture.

Where to Begin

To see what this approach might mean in your plant, start by articulating your competitive strategy. Are you competing on price? Time to market? Quality? There will always be trade-offs. If you ask 10 people at different levels of your company what they believe to be the company’s business strategy, will you get the same answer?

Advanced automation and IT can help you implement strategies in five main areas: improving production value, reducing raw material and energy costs, and improving plant safety and regulatory compliance. If none of these factors plays into your business strategy, technology investments might not be justifiable for you at all. But if you can clearly define success in any of these areas, determining the role of automation and information technologies in bringing about that success should be much easier. It will take some directed effort—including defining the contributions of systems and individuals throughout the company, and enabling real-time views of progress—but the results will be more than worth it.