Lean Laggards: Exploring the State of Lean in Pharma

Pharma companies continue to face challenges of globalization, complex supply chains and hyper-competition - all while demand for treatments continues to increase. As a result, the need for greater throughput, higher quality and reduced costs has become a top priority.

Over the last two decades, lean programs have become a popular approach to addressing these challenges in the pharmaceutical industry, as evidenced by the number of published case studies, conferences devoted to the topic and published articles. Unfortunately, the industry has seen little overall progress in becoming more “lean,” as indicated by the lack of improvement in inventory turns performance. In recent years, performance across the industry has lagged that of the previous decade with gains not appearing to be sustainable due to a widespread lack of understanding of lean’s strategic value at the senior leadership level, and how it should be optimally applied.

INVENTORY TURNS AS A LEAN METRIC

Lean is a business improvement approach that focuses on process improvement in new product development, manufacturing and distribution in order to cut lead times, improve quality and customer responsiveness, resulting in enhanced revenues, reduced investment and costs. Pioneered by Toyota in the 1950s and widely adopted across industries, lean’s objectives include using less human effort, less inventory, less space and less time to produce high-quality products as efficiently and economically as possible while being highly responsive to customer demand.1

Although there is no universally accepted measure of a company’s “leanness,” inventory turns are a reliable indicator.2 The trend of inventory turns over time indicates how well a company is progressing in terms of becoming more lean and improving its processes. Lower levels of inventory directly correlate to improvement in the competitive edge factors of speed, quality and cost. That’s why the companies that have successfully implemented lean have focused intently on reducing inventory, sometimes characterizing inventory as “evil.” Similarly, noted lean experts such as Richard Schonberger view inventory as a catch basin for a multitude of business ills.3

In addition, inventory is a standard financial metric and is readily comparable company-to-company, as well as over time within a business. It is also highly visible - walk around a facility characterized by high levels of inventory and you can conclude that the facility is not lean.

HISTORICAL CONTEXT

Historically, the pharmaceutical industry has ranked at the very bottom in terms of the trend of inventory turns improvement.3 The pharma industry has been a late adopter of lean, due to the lack of a “burning platform” for change. In the 1990s when profit margins were at historic highs, little attention was paid to the competitive edge elements of speed and cost with the focus of money and resources on R&D rather than operations.

The little attention that operations did get was focused on compliance rather than process improvement.4 The standard practice of ensuring that more than enough of each product was available to meet customer needs coupled with a lack of attention to operational efficiencies led to excessive inventories. Further, the sales and market-share strategy of pushing more and more inventory into the pipelines also drove up inventories.

At the end of the 1990s, new pressures began forcing a change in mindset. The government and society exerted tremendous pressure on pharmaceutical companies to reduce costs and improve quality. As more brand drugs lost their patents in the 2000s and early 2010s, price increasingly became a key competitive factor. With globalization and modernization, demand for mission-critical treatments dramatically increased with capacity constraints becoming more commonplace. In addition, the global counterfeiting of drugs increased the regulation of safety and quality.

As the 1990s ended and the new century began, pharma companies such as Pfizer, AstraZeneca and GSK increasingly looked at lean as an approach to address these challenges by driving improvements in cost, quality and supply.

REVISITING LEAN'S PROGRESS: SEVEN YEARS LATER

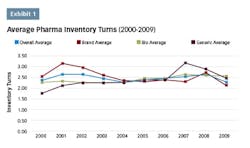

An analysis performed in 20105 utilizing data from the top pharmaceutical companies by revenue on the trend of inventory turns indicated that the average inventory turns remained essentially flat over both the previous five- and 10-year periods. While there were some companies that had shown improvement, there wasn’t a strong enough trend to draw definitive conclusions.

A follow-up analysis was recently completed to determine whether there has been any improvement over the last seven years since the previous analysis. The top 20 pharma companies by revenue are listed in chart 1, along with their inventory turns for the corresponding annual period. The average inventory turns for these companies is also shown.

The overall trend in inventory turns has not changed since the previous analysis period seven years ago. Only Amgen has shown a consistent upward trend over this time frame. Gilead Sciences has shown progress since 2012, but given this short time frame it is likely premature to draw meaningful conclusions. Aside from these two companies, there aren’t any companies in this data set that show a strong upward trend, indicating that the status quo for the pharma industry has not changed from the last time this analysis was completed.

While some progress has been made in the industry in this century, it has clearly been incremental rather than industry changing. In the last 10 years, pharma has improved its inventory turns performance relative to other industries,6 however, it still ranks near the bottom relative to other industries. And while there is a plethora of published success stories, it appears that these successes have not been enough to “move the dial” for pharma companies for their overall company inventory turns.

Finally, it appears that where lean has been successfully applied in the pharmaceutical industry, progress has not been sustainable. While in the 2000s there were a small number of pharma companies such as Johnson & Johnson and AstraZeneca that did exhibit an upward trend in inventory turns, since that time these leaders have not shown continued progress, and in some cases have regressed. Utilizing the inventory turns metric, it is difficult to find many pharma companies that have made sustainable progress with lean initiatives, with only a few companies on the short list, including Amgen and several smaller revenue companies such as Juniper Pharmaceuticals and Atul Pharmaceuticals.

WHY HAS THIS HAPPENED?

What can explain the dichotomy between the published lean success stories and lack of sustainable progress? There are several potential causes that can be linked together by a common theme: a lack of full understanding of lean’s strategic value, and how it should be applied to recognize its full potential and ensure sustainability.

Lack of Senior Management Commitment.

Lack of senior management focus and commitment is a widely accepted reason given for lack of successful implementation and success of virtually every type of business improvement initiative, including Six Sigma, Agile Manufacturing, Employee Engagement, ERP, Reengineering, etc.4 The most successful improvement initiatives are driven by top management, e.g., Jack Welch at GE or Larry Bossidy at Allied Signal, and are driven top-down on a company-wide basis, across departments, functions and geographic borders. However, in the pharma industry lean initiatives are typically applied in an isolated manner, i.e., in one manufacturing facility or solely in manufacturing operations, rather than as a concerted effort across an entire company as Six Sigma was done at GE.

Pharma industry executives do not appear to see lean as being strategic enough to warrant their attention and thus are not actively involved in the change - a prerequisite for success.

A word search of the annual reports for the top pharma companies by revenue from 2014-2016 was conducted. The terms included “lean,” “Just-In-Time,” “Operational Excellence” and “Continuous Improvement.” For 12 of these companies, none of the searched terms were found and of the remainder, only two companies, - Amgen and AstraZeneca - drew any meaningful connection between these initiatives and strategic benefits.

The minimal mention of those terms suggests that most pharma executives have little concern for lean-related initiatives and feel that the investment community would not either. When pharmaceutical executives perceive lean as worthy of initial support, but not strategic enough to warrant continued attention, they may turn to other items deemed more strategic. As a result, lean implementations can fail, or in the case of successful implementations, performance can regress.

One example of a company that in recent years has successfully bucked the trend is Amgen. On the first page of the 2016 Letter to Shareholders, the CEO, Robert A. Bradway, directly links the company’s focus on OpEx to earnings and margin improvement over the last few years. In their communications, Amgen touts their transformation program and the use of Continuous Improvement (CI) tools as a “core capability and a competitive advantage.”

Since 2009, Amgen has demonstrated an upward trend in inventory turns of 6.54 percent, which translates directly into free cash flow improvement of the same rate. These funds can be spent on product development, equipment, pay increases, share buybacks, dividends, etc. When measuring the success of a lean program, if the company’s progress isn’t accompanied by a significant upward trend in inventory turns, lean isn’t being applied correctly.

“Operations only” focus.

The vast majority of lean implementations in the pharma industry appear to be isolated to manufacturing operations drastically limiting lean’s potential value. A recent manufacturers-only study6 divided total inventory for each company into its components: purchased/raw material (RM), work-in-process (WIP) and finished goods (FG). In this study, improvement showed up only in the WIP percentage, i.e., internal manufacturing related processes, which is evidence of lean initiatives solely focused in manufacturing operations. Successful application of lean across the supply chain would be evidenced by reduced inventory in all areas.

Over the last two decades or so, there has been an increased amount of activity in the pharmaceutical industry to outsource production to Asia in pursuit of lower costs. An increasing number of Asian contract manufacturing organizations have been securing more outsourcing orders from large pharmaceutical companies. While labor costs are significantly lower in Asia (although they have been steadily rising over the last few years), outsourcing has brought on a new set of challenges, specifically lengthening and adding more complexity to the supply chain and quality issues - elements completely at odds with the goals of lean. In addition, lean adoption has been much lower in Asia,7 which means there is much less likelihood of outsourcing to a facility that will have the same level of leanness as in the United States., resulting in a loss of the lean gains that have been achieved in the past.

Along with work-in-process inventories, pharma industry supply chain inventories (raw materials and finished goods) have been growing, which is evidence of lack of overall supply chain leanness. The longer overseas transportation times issue is frequently addressed by building more inventory in the supply chain, which only results in more quality issues and excessive costs in the areas of inventory, warehousing and transportation. While outsourcing to Asia has resulted in lower labor costs, the net benefits appear dubious. Focusing on applying lean solely in one node of the supply chain greatly limits the potential value.

Another key segment of the pharmaceutical value chain that has received little attention is applying lean to product development. The potential value here is enormous: every day saved in bringing a major new drug to market is worth nearly $250K in cost savings and more than $1 million in revenue; a month is worth $7.6 million in cost savings and tens of millions in revenue.8 Other industries have successfully applied lean to product development and achieved tremendous success with Best in Class performers able to bring products to market 25 percent faster on average.9 While there are case studies of application of lean to pharma product development, these are few and far between, likely due to a lack of recognition of the potential to apply lean in this area and how to do so within the pharma environment.

Cost reduction focus.

When properly implemented, lean results in strategic, financial and operational benefits in the areas of speed, quality and customer responsiveness. However, when reviewing lean case studies in the pharma industry in goals of the program and benefits achieved, cost reduction is typically the primary value driver, with other benefits such as quality and supply receiving secondary mention. Why is the cost focus mindset so prevalent? Labor costs are easy to measure, while the strategic benefits of improved speed, quality, flexibility and customer satisfaction are more challenging to quantify. Executives justify their support of initiatives based on financial results, and labor costs are the easiest to quantify. Even the traditional language of business cases shows this bias - benefits are typically listed as “savings,” which imply cost reduction.

While the primary focus on cost reduction is evident across industries, it is more prevalent in the pharma industry in part due to legacy culture issues. Moving beyond cost reduction to benefits in revenue enhancement requires cross-functional collaboration, for example, marketing, sales and operations and sales working collaboratively to increase market share by capitalizing on enhanced speed and increase capacity, or operations and product development collaborating on building quality into new treatments. Yet pharma functions, divisions and geographic units remain strongly independent with the silo mentality deeply entrenched at most drug companies. This lack of collaboration also drives the isolation of application mentioned earlier to one part versus the entire supply chain. Lean cannot be delegated by pharma company leadership - culture change needs to be driven top-down by senior leaders.

There is a lot to be gained by companies in the pharma industry by implementing lean. As few pharma companies have been able to implement sustainable lean, a pharma company that focuses on lean as a strategic tool will clearly have advantages over its competitors and can capture additional market share. While the challenges to successful lean implementation may seem daunting, they are not insurmountable.

Editor’s note: In part II of this series, the author will discuss what pharma companies can do to address these challenges to ensure their lean efforts are successful and sustainable over the long term.

References

1. Spector, R. “How Constraints Management Enhances Lean and Six Sigma,” Supply Chain Management Review, January/February 2006.

2. Spector, R. “The Impact of Inventory Turns on Speed, Quality, and Costs,” Pharmaceutical Manufacturing, June 2009

3. Schonberger, R. Best Practices in Lean Six Sigma Process Improvement – A Deeper Look (Hardcover), (Wiley & Sons, 2008)

4. Spector R., West M., “The Art of Lean Program Management,” Supply Chain Management Review, September 2006.

5. Spector, R. “How Lean is Pharma?”, Pharmaceutical Manufacturing, July/August 2010.

6. Schonberger, R. “Cycles of Lean: Findings from the Leanness Studies--Part 2,” Management Accounting Quarterly, 18/1, Fall, 2016: 18-27.

7. Schonberger, R. “Cycles of Lean: Findings from the Leanness Studies--Part 1,” Management Accounting Quarterly, 17/4, Summer, 2016: 21-33.

8. Tufts CSDD. “Quantifying Savings from New Drug R&D Efficiencies”, Parexel’s Bio/Pharmaceutical R&D Statistical Sourcebook 2006/2007

9. Aberdeen Group. “The Lean Product Development Benchmark Report,” May 2007.