CDMO Industry Thrives Amid Consolidation

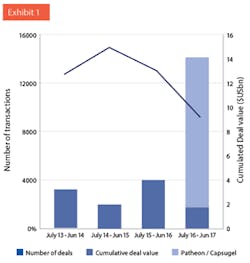

Transactions targeting CMOs located in the US, EU25 or Canada. Line: Number of deals reported. Bars: Cumulative deal values as reported. Note: Acquisitions of Capusgel and Patheon both closed after June 30, 2017. (Source: KP Research, MergerMarket, ThomsonReuters, FiercePharma.)

The summer saw two of the largest M&A transactions ever in the CDMO industry: Lonza’s acquisition of Capsugel for $5.5 billion, and ThermoFisher taking over Patheon for $7.2 billion. These two transactions combined are bigger than all transactions in the past four years (see Exhibit 1). The deals are salient examples of two trends: First, the ongoing consolidation among CDMOs. Second, the entrance of new players to the market.CONFLICTING VIEWS ON PHARMA OUTLOOKWhen discussing the outlook of the pharma industry, there are conflicting views. On the one hand, global spending on medicine is expected to grow by a healthy 4% to 7% per year, increasing by 50% to $1.5 trillion in 2021.1, 2 Growth is driven by innovation and new launches. Intensity of R&D has increased over the last decade: In 2016, twice as many clinical trials were ongoing than in 2001 (12,300 vs. 6,000). As a result of the biotech revolution of the past decades, biologics will make up 50% of the top 100 drugs by 2021.2 The boom of venture capital funding means that growth will be fueled by smaller innovators (or “biotechs”); the top 10 originators are supposed to lose market share in the developed markets in the next five years.2On the other hand, pressure to correct unjustifiable prices of older drugs is increasing, and questions about huge price differences between the U.S. and other parts of the developed world4 become more widely discussed. The latter point is particularly pertinent since a substantial part, in absolute terms, of the anticipated growth is expected to be created in the U.S.: Americans are expected to spend $200 billion more for drugs in 2021 than in 2016.1 On the other end of the spectrum, the price level for generics seems to be unsustainably low, given that drug shortages have become more common.Costs of drug development is steadily increasing5, which means that medium-sized pharma companies struggle to keep up a sustainable drug development pipeline. Classical innovation - developing new active principles - is becoming unaffordable for most pharma companies, which has fundamental consequences for the industry. We anticipate that pharma companies will finally coalesce around one of four strategic archetypes: originators, point-of-call specialists, low-cost providers and OTC/consumer health. Amongst many other areas, cost pressure on manufacturing will certainly increase, also for high-margin original drugs.CDMOs/CROs GROW FASTER THAN PHARMA

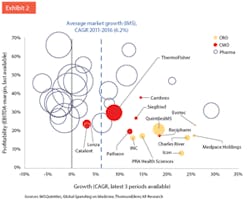

Profitability (% EBITDA-margin) vs. growth (CAGR revenue growth) of CMOs and CROs vs. large Pharma companies. Bubble size indicates revenues in the last year.

Against this backdrop, the CDMO industry is thriving. CDMOs collectively generate approximately $40 billion in revenues6 and the market is forecast to grow by 5%e6 to 6.5%7 in the next five years. Future growth has two fundamental drivers: First, most of the small pharma innovators do not want to lock in capital to build manufacturing plants, but rather rely on CDMOs. Second, outsourcing by Big Pharma is expected to further increase, from an “outsourcing penetration” of 30% today to 40% in 2020. Combined with the anticipated volume growth, this promises a substantial expansion of the addressable market for CDMOs.Pharmaceutical companies are still much more profitable than their service providers; the Big Pharma companies grew more slowly than the market, i.e., they lost relative market share (see Exhibit 2). CDMOs, however, grew more quickly than the market, and significantly faster than many of their Big Pharma clients. For comparison, we also inserted some of the large CROs, which also grew substantially faster than the pharma market.

IN A FRAGMENTED MARKET, BIAS FOR LARGER PLAYERS

Despite the considerable number of transactions, the CDMO market is still very fragmented. The top five players generate approximately 15% of the $40 billion total, and there is a long tail of medium-sized and smaller companies - we count at least 300 CDMO companies competing in the market.

However, there is a strong bias for larger firms: pharma clients want long-term, reliable relationships and will favor large CDMOs over smaller ones (similar to the “size affinity” between pharma companies and CROs⁸). Also, large CDMOs have the capacity and means to manage and cultivate complex niche technologies which they can offer to their clients.

Fragmentation, growth and size bias make an industry prone to consolidation, and attractive for new entrants. Private Equity Groups have played a strong role in building the CDMO industry (as well as for CROs), and last year again saw several transactions involving PEGs buying out CDMOs, most notably AMRI. In addition, firms in related industries, such as ThermoFisher, are attracted to the CDMO industry. The table gives examples of recent acquisitions of CDMOs by strategic buyers and private equity groups.

Examples of new entrants in the CDMO market in the last two years

BIOPHARMA CONTRACT MANUFACTURING

Prime examples of complex, capital-intensive manufacturing processes are those related to biologicals. Even some of the largest pharma companies prefer to enter into strategic alliances with specialist CDMOs, rather than building manufacturing plants on their own, as exemplified by Sanofi’s $285 million alliance with Lonza announced this year.

Biopharmaceutical toll manufacturing and biosimilar development overlap. For example, Samsung Biologics offers contract manufacturing services and has developed several biosimilars, in partnership with large biotech companies. Samsung Biologics is also an example of a successful new entrant into the CDMO market - with anticipated volume of 362T liters for mammalian cell culture, it will be the largest biopharma CDMO by 2018. The company went public in November 2016 and on Sept. 1, 2017, traded at a valuation of more than $16 billion.

The biopharmaceutical CMO market is an oligopoly in which Samsung Biologics, Lonza and Boehringer have the lion’s share, which makes it attractive for new entrants: Japanese Asahi Glass acquired CMC Biologics at the end of 2016; and KBI, subsidiary of Japanese group JSR, acquired two companies to expand its biopharmaceutical contract manufacturing capabilities.

An intriguing question is how manufacturing of cell-based treatments such as CAR-T cells will develop. Manufacturing costs of these “revolutionary” therapies are a major issue.9 While pioneer Novartis keeps CAR-T cell production in-house, and in 2013 even acquired a facility from Dendreon, Lonza acquired PharmaCell to complement its capabilities to provide services for autologous cell therapy manufacturing.DAWN OF PHARMACEUTICAL-CMO ALLIANCES?Pharma companies have been relying on acquisition of, or in-licensing from, biotech companies for innovation. In 2011, McKinsey, a consultancy, suggested that, like the automotive industry, other parts of the pharma value chain may disintegrate, with few large brand-owners sourcing everything - from innovation to manufacturing - through a network of suppliers. Along these lines, in the first half of this decade, Big Pharma companies established strategic alliances with CROs, establishing preferred relationships with few (2-3) CROs instead of deciding case by case (or trial by trial) with whom to work.10The same may happen in manufacturing. The large CDMOs may soon be big, stable and broad enough to cover substantially all manufacturing needs of Big Pharma companies. We believe this is one reason for Lonza’s acquisition of Capsugel - complementing existing technical capabilities and gaining scale. Similarly, Patheon becomes part of a large group under Thermo and hence may be viewed as a more stable partner for Big Pharma companies.

Clearly, given the many technical and regulatory constraints, transformation of a manufacturing network takes much more time to implement than changing suppliers of services. However, the transfer of manufacturing units, from pharma company to its future CDMO, could accelerate the process - thus the future of the CDMO industry may resemble its beginnings in the mid-90s.e11Kurmann Partners AG is a global M&A advisory boutique for mid-market transactions in the pharmaceutical industry. Among the firm’s specializations are transactions involving pharma manufacturing sites. See www.kurmannpartners.com.

REFERENCES

1. IMSQuintiles, Outlook for Global Medicines through 2021. 2016.

2. EvaluatePharma, World Preview 2016, Outlook to 2022. 2016.

3. Crow, D., Pharmaceuticals: Staying power, in Financial Times. 2016, @FinancialTimes.

4. Goldstein, D.A., et al., Global differences in cancer drug prices: A comparative analysis. Journal of Clinical Oncology, 2016. 34(18_suppl): p. LBA6500-LBA6500.

5. Avorn, J., The $2.6 billion pill--methodologic and policy considerations. N Engl J Med, 2015. 372(20): p. 1877-9.

6. Patheon, Presentation at JP Morgan Healthcare Conference. 2016.

7. Recipharm, Presentations at 2016 Jefferies Health Care Conference. 2016.

8. Finding Alignment - Opportunities and Obstacles in the -Pharma/CRO Relationship. 2012.

9. Manufacturing costs loom large for personalized CAR-T cancer meds and their need for speed | FiercePharma. 2017.

10. Hughes, J. and S. Price. The Perils and Promise of Strategic Partnering with CROs. 2017.

11. Miller, J. Contract Manufacturing Through the Years. 2017.